If Fixed Costs Do Not Change Then Marginal Cost

If fixed cost do not change the marginal cost. If you were to get a score of 80 on your next exam this score would pull your average down and your new average.

Marginal Cost Definition Formula And 3 Examples Boycewire

Fixed and variable costs are key terms in managerial accounting used in various forms of analysis of financial statements Analysis of Financial Statements How to perform Analysis of Financial Statements.

. Cost and marginal cost is only affected by the variable cost portion of total cost. To reduce a companys break-even point you could reduce the amount of fixed costs. If fixed costs do not change then marginal costA also remains constantB equals the change in variable cost divided by the change in output.

If fixed costs do not change then marginal cost. The change in the total cost is always equal to zero when there are no. If fixed costs do not change then marginal cost equals the change in variable cost divided by the change in output.

Equals the change in variable cost divided by the change in output OD. Mathematically marginal cost is the first derivative of the cost function. Fixed costs are expenses that have to be paid by a.

Variable Costs Variable costs are expenses that vary in proportion to the volume of goods. If the fixed costs were to double the marginal cost of production is still zero. View the full answer.

Since fixed costs are by definition a constant changes in them will not affect marginal cost. Equals the change in average fixed cost divided by the change in output. The single firms supply curve is defined as it marginal cost as long as MC is above it average cost A firm would not sell below its average cost since it would loae money Mathmatically we can define for the single firm S MAX AC MC Our basic assumptionfor this discussion is that MC 0.

Beside above what happens to break even point when fixed costs increase. In the world oil market oil is supplied up to the point where the marginal cost of the last barrel is just equal to the price buyers are willing to pay for that last barrel. It is calculated by taking the total change in the cost of producing more goods and dividing that by the change in the number of goods produced.

B that at some point adding more of a variable input to a given amount of a fixed input will cause the marginal product of the variable input to decline. What is the relation. Variable costs and expenses increase as volume increases and they will decrease when volume decreases.

C equalsthe change in average variable cost divided by the change in outputD equals the change in average fixed cost divided by the change in output. The BalanceMarina Li. Equals the change in average.

A change in your fixed or variable costs affects your net income. Bequals the change in average fixed cost divided by the change in output. Advertisement New questions in Business.

Marginal costs are a function of the total cost of production which includes fixed and variable costs. Intuitively the cost of producing an additional unit of output is independent of fixed costs which have already been incurred. For example if a product costs 10 to produce and the fixed cost goes up to 25 then marginal cost.

Assume that your average grade in a course is 85. Cost is the affecting component as changing fixed. When you operate a small business you have two types of costs - fixed costs and variable costs.

Contrast to what we would normally think changes in fixed costs do not affect marginal cost. Fixed costs do not change with the amount of the product that you produce and sell but variable costs do. Rather than think about costs think about grades on a series of exams.

Also remains constant OB. Fixed throughout the level of production which means that fixed cost does not affects marginal. C equals the change.

Examples of fixed costs are rent and insurance payments property taxes and employee salaries. Fixed costs do not change with increasesdecreases in units of production volume while variable costs fluctuate with the volume of units of production. If fixed costs do not change then marginal cost A equals the change in variable cost divided by the change in output.

If fixed costs do not change then marginal cost O A. When fixed cost is not changing the marginal cost is calculated by dividing the difference in total cost by difference in output. Fixed costs and fixed expenses are those which do not change as volume changes.

Is important because it clarifies that when marginal cost needs to be changed then only variable. The change in total cost which arises due to the increment in the cost of produced good by one unit is termed as marginal cost. Fixed costs do not affect marginal cost.

It also affects your companys breakeven point. The term fixed cost refers to a cost that does not change with an increase or decrease in the number of goods or services produced or sold. Marginal cost represents the incremental costs incurred when producing additional units of a good or service.

Jill Johnson owns a pizzeria. The relationship between average and marginal cost can be easily explained via a simple analogy. Fixed costs of production are constant occur regularly and do not change in the short-term with changes in production.

Under the basic assumption and that costs are. Equals the change in variable cost divided by the change in output. Cequals the change in average variable cost divided by.

Equals the change in average variable cost divided by the change in output. If fixed costs do not change then marginal cost Aequals the change in variable cost divided by the change in output. Equals the change in average fixed cost divided by the change in output OC.

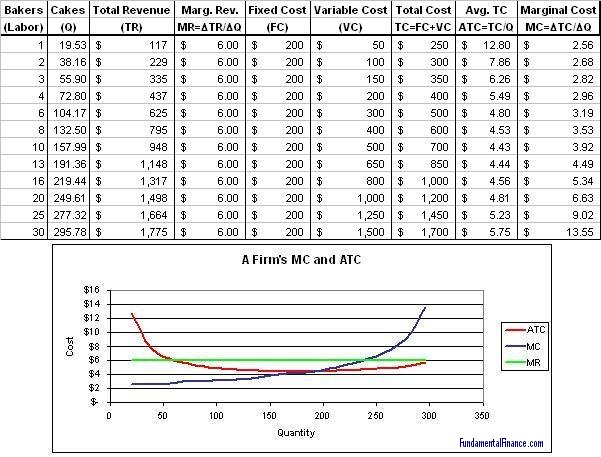

Marginal Cost Average Total Cost Fundamental Finance

Amosweb Is Economics Encyclonomic Web Pedia

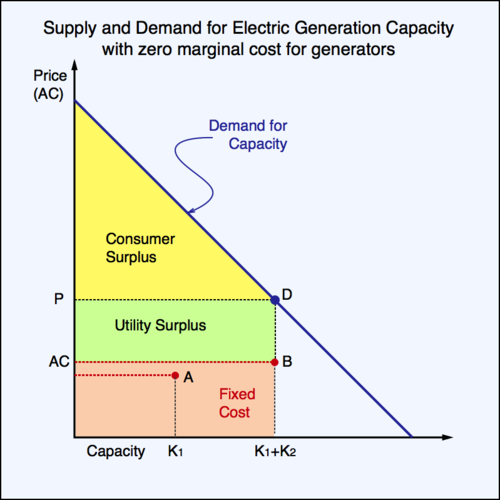

Energy Economics With Zero Marginal Costs

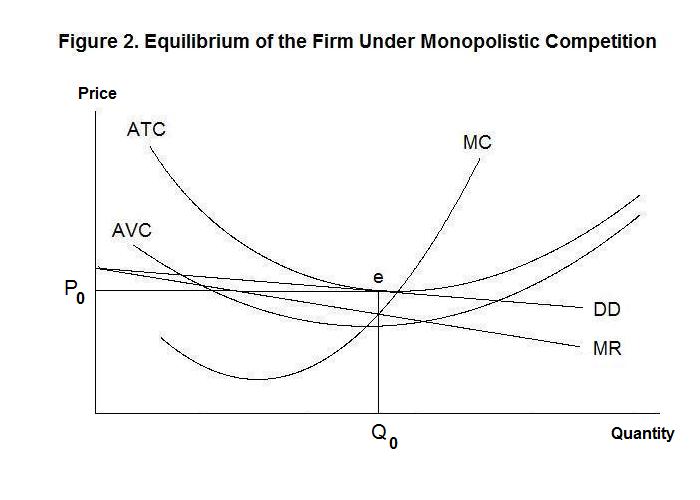

The Firm Under Competition And Monopoly

No comments for "If Fixed Costs Do Not Change Then Marginal Cost"

Post a Comment